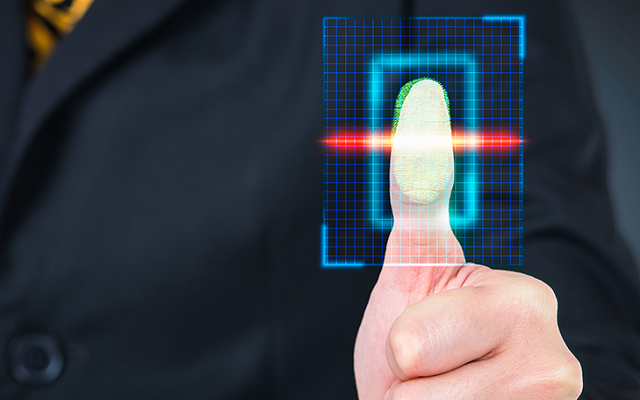

Biometric Verification: Implications for Over the Counter Money Transfer in Pakistan

The State Bank of Pakistan, in July 2016, developed regulations on necessitating biometric verification for over the counter money transfers in Pakistan. These regulations, part of the updated branchless banking regulations of July 2016, have improved compliance to transparency, tracking, and the efforts of the regulator to curb money laundering and terror financing. This is a significant shift from the previously required Centralized National Identification Number (CNIC) verified money transfers, where an individual would provide his/her original CNIC to the agent for transferring money to another CNIC, throughout Pakistan. After the introduction of the Biometric Verification System (BVS) regulation, customers now need to verify each transaction through their fingerprint, both at the sending end and the receiving end.

The deadline for implementing the BVS at all agent outlets for the currently operational branchless banking networks in Pakistan was 30th June 2017. In complying with the deadline, at present, EasyPaisa and JazzCash, who maintain the two largest agent networks in Pakistan have reportedly enabled more than 50 percent of their agents to provide BVS supported services across Pakistan. Both, EasyPaisa and JazzCash are currently working to enable the remaining retailers to provide BVS supported services and have planned to build this capacity for their top retailer locations first.

Biometric Verification: Implications for Over the Counter Money Transfer in Pakistan

At the backend, the BVS devices connect to an android tablet which communicates through the Data SIM (using GPRS, Edge, 3G and 4G). This information is than integrated with the branchless banking and NADRA systems, to verify each transaction in real-time. This new technology is likely to impact the industry in both positive and negative ways.

It is likely that mobile account registrations will increase as branchless banking agents, after taking consent of the individuals, may register customers for a mobile account who do not previously have such an account but come to a service provider for a money transfer. The digital financial service providers believe that an increased number of mobile accounts will eventually decrease the total cost of commissions. Also, due the availability of BVS devices at a greater number of retail outlets, SIM card selling locations have increased, resulting in greater convenience to GSM customers throughout the country.

Through BVS technology, stricter controls on fake and fraudulent practices can be ensured at both the sending and receiving ends and it can also ensure enhanced anti money laundering scrutiny in case of such transactions. The customers will now be more protected as the chance of money landing into an unauthorized receivers’ hands is eliminated. Higher transaction limits are available to customers – PKR 50,000 per month with BVS of sender, PKR 50,000 per month with BVS at both sender and receiver end – resulting in further benefits, such as enhanced business activity, increased convenience for customers etc. On the other hand however, the cost for the operator and the consumer has increased, due to added cost [1] of verification by NADRA for each transaction and the costs associated with the implementation of BVS devices at thousands of agent locations. The retailer trainings and device maintenance can also result in digital financial service providers having to spend much more in the initial stages. In the short term, the total number of money transfer transactions are likely to decrease as all agents currently do not possess the BVS devices. Also due to lack of knowledge and training, many retailers switch off their devices to save on battery life, not realizing that re-starting the BVS device would take time which means longer wait time and customers getting discouraged.

The system also means increased dependency on connecting with the NADRA database and high speed internet connectivity is required to make this technology work efficiently. This may become a challenge in the long run for mobile money providers.

PTA Taxes Portal

Find PTA Taxes on All Phones on a Single Page using the PhoneWorld PTA Taxes Portal

Explore NowFollow us on Google News!